According to a recent Ipsos report, 59% of people think that companies aren’t working hard enough to combat climate change. And 71% believe businesses “use environmental claims without committing to real change at least occasionally.” This is despite the fact that in recent years, corporations have lined up – one after another – announcing big public commitments to combating climate change.

Amid all the perception and posturing, it can be hard to locate the truth. Are we stuck in a cycle of greenwashing? Or are substantive changes on the way?

To understand what’s really happening, looking at innovation activities is helpful. Most industries will need substantive technological innovation to meet carbon-neutrality targets: the adoption of sustainable aviation fuels in the airline industry, biobased feedstocks in the chemicals industry, sustainable battery technologies in the automotive space, and so forth.

Wellspring conducts an annual research study into corporate innovation practices, affording us an uncommonly nuanced view of such questions. For our 2023 R&D and Innovation Agenda report, we surveyed 330 mid- and senior-level corporate innovation professionals. We also interviewed dozens of R&D and innovation leaders to understand the qualitative trends underlying the data.

Across all our interviews, climate change was one of only three topics featured prominently in nearly every conversation (the others were AI and the economy). Regarding current decarbonization efforts, there were three big takeaways.

From maybe to mandate

Climate change is hardly a new priority among corporations, and neither are the charges of greenwashing that go with it. In the recent past, although there has been some desire to reduce carbon emissions, the leadership at most companies was either unwilling or unable to make decarbonization a top priority.

This year, we heard a different story: tackling climate change has become a mandate. In previous years, most firms’ market research data indicated that consumers, despite caring about sustainability, were unwilling to pay a premium for greener products. Fast forward to 2023, and that outlook has evolved substantially. In many food and beverage categories, brands have found they must make progress on carbon emissions or risk being punished by consumers. Consumer electronics companies have begun to build sustainability into their cost profile and their pricing. Many firms expect the regulatory environment to begin mandating carbon neutrality sooner rather than later, probably starting in Europe.

These effects have begun to exert an influence through the value chain. Companies that are feeling pressure from consumers and regulators are in turn, making demands of those in their network. OEMs that have already made substantial progress on Scope 1 and Scope 2 compliance have now set their sights on Scope 3 – in which both their upstream and downstream supply chains must also demonstrate carbon neutrality. Many large B2B suppliers are now executing dedicated emissions reduction plans, with the understanding that doing nothing will ultimately cost them their largest customers. There is a general sense that these ripple effects, while just now coming into the foreground, appear to be accelerating.

Growing pains galore

Although most corporations are taking climate change more seriously, they are still learning how to execute it. For example, many firms have taken the step of appointing a Chief Sustainability Officer or ESG Director. Yet these new “climate czar” positions are generally coordinating the response more than driving it. They are serving as a PMO that reports on progress, provides documentation, and submits regulatory filings. Meanwhile, the real investment decisions and execution muscle reside elsewhere in the company.

The R&D function in particular, has been directly implicated in the upswell. In 2023, many R&D teams were given a new directive from top executives. They must innovate technological solutions toward net-zero emissions, working in concert with key operating functions such as Manufacturing and Distribution. This committed push to decarbonize is welcome news for many – as many R&D and innovation professionals have been fretting privately about the lack of climate progress.

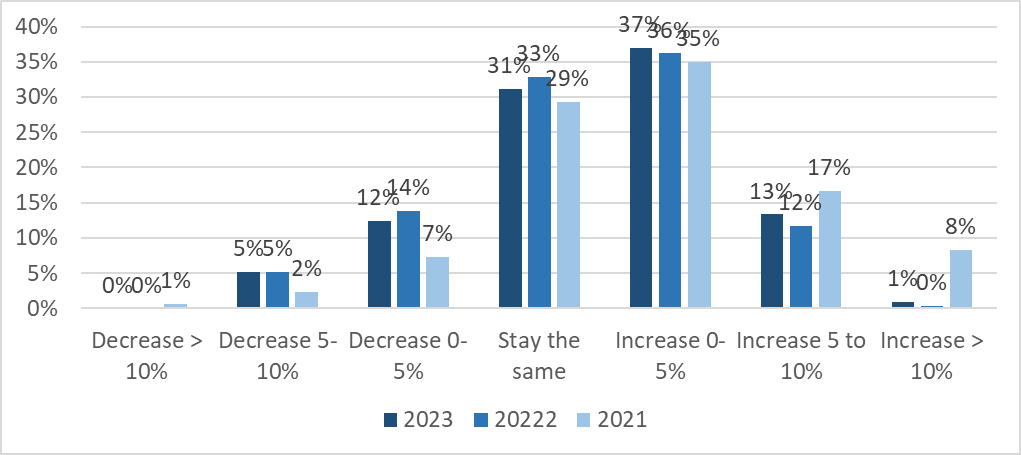

But it is also a double-edged sword. R&D teams have effectively added a complex new mission to the innovation portfolio, forced to shift resources on the fly to demonstrate progress. There has yet to be a commensurate increase in budget or headcount. Per our 2023 study data, most firms saw, at best, a modest rise in innovation spending (see Figure 1) – which has barely kept pace with recent inflation. Interviewees told us that rarely, if at all, was this modest uptick earmarked specifically for climate-change initiatives. For now, in too many cases, it is yet another example of “do more with less.”

In many industries, there is also the lurking issue of the cost and complexity of implementing change – even once the core technologies are available. Especially in sectors with a heavy physical equipment or manufacturing footprint, meeting net-zero targets will entail replacing expensive machinery on a global basis. The natural replacement cycles are often measured in decades, which makes the curve cost-prohibitive, not to mention the logistical challenges of refitting worldwide operations on an accelerated timeline.

A still-forming ecosystem

Despite these difficulties, most executives who participated in our research were optimistic that the decarbonization momentum would continue deepening and that many of the current “unsolvable” challenges – technical or balance sheet related – would prove solvable over time.

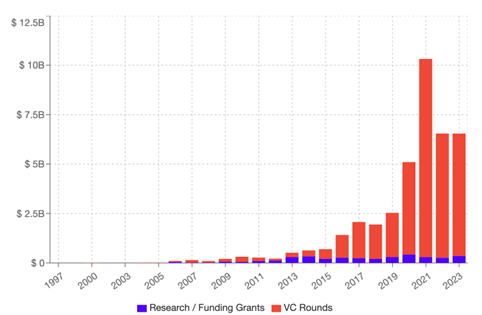

One reason is that there is a fast-evolving provider ecosystem coming online to serve the heightened corporate demand for sustainability solutions. Anticipating some of the developments described above, recent years have witnessed substantial venture investment flowing into technologies ranging from carbon capture to synthetic biology and more (see Figure 2). Although the capital markets have cooled overall in 2022 and 2023 due to structural economic concerns, the funding levels for emissions-reduction technologies are still robust and are likely to remain strong for the foreseeable future.

Figure 2: Venture and basic research funding for carbon capture (left) and synthetic biology (right). Source: Wellspring Scout.

The service provider landscape has also been taking major strides forward. The need for auditing and formalized assessments of a company’s carbon footprint continues to grow, and along with it comes a larger and more sophisticated set of capabilities in the marketplace. Although everyone expects government reporting requirements to increase in the years to come, perhaps the biggest driver of these services today comes from other companies. Large multinational brands already require their suppliers to show accredited proof of the strides they’ve taken to reduce their emissions.

As with most trends in the carbon-neutrality game, it’s two steps forward and one step back. While recognizing the need for objective standards and accountability, the fees for carbon footprint audits add another large expense to balance sheets that are already struggling to absorb the necessary innovation investments. Furthermore, many leaders worry that we may measure the wrong things. If everyone focuses on net-zero emissions, will there also be accountability for removing “forever chemicals” and achieving circularity – or will we just be swapping one set of problems for another?

Compared to the recent past, these are good problems to have. A few years ago, the mainstream of the corporate world was still waiting in the wings. As companies have begun to tackle climate change with purpose and intent, growing pains will inevitably emerge. But make no mistake: the general trajectory is upward.